myCSUSM

myCSUSM

1098-T FAQs

- What is Form 1098-T?IRS Form 1098-T (Tuition Payments Statement) provides information to students, from educational institutions, which may be used in determining a student’s eligibility for tax credits.

- Am I eligible to receive a 1098-T?

More information about Education Tax Credits and eligibility can be found at Form 1098-T Information.

- When will I receive my Form 1098-T?1098-T statements are made available no later than January 31st each year.

- How will I receive my Form 1098-T?Most all students opt-in to receiving their 1098-T in electronic format only. The electronic version can be accessed from Student Center via MyCSUSM. For students who may have opted-out of receiving an electronic version, a paper Form 1098-T will be mailed to your mailing address no later than January 31st. If you don’t have a mailing address on file, it will be sent to your home address. If neither of those address types are on file, it will be mailed to your campus address.

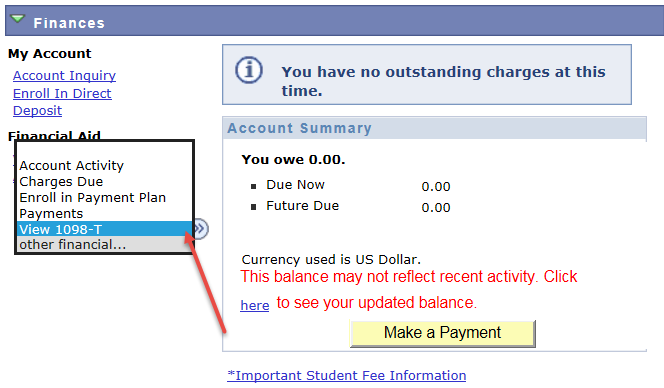

- How can I access my Form 1098-T online?

If eligibility requirements are met, you may obtain your 1098-T form online by utilizing the following steps:

- Log in to your MyCSUSM account and access your Student Center.

- Click the “View 1098-T” link in the “Finances” section of your Student Center.

-

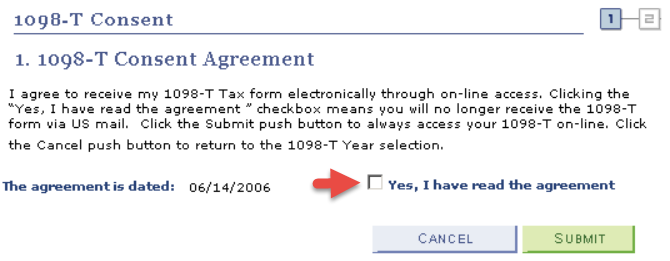

If this is your first year at CSUSM, you will be asked to consent to receiving your 1098-T online

-

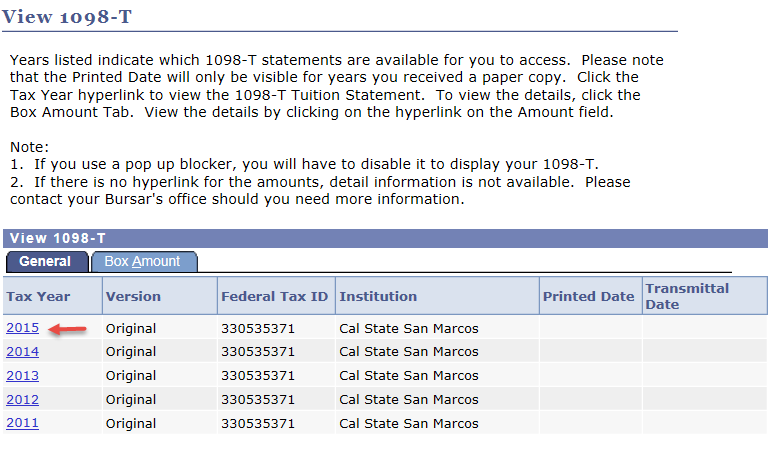

Click the link for the year you would like to view and print

- Log in to your MyCSUSM account and access your Student Center.

- I misplaced my original Form 1098-T, can I get a replacement?Yes, by contacting Student Financial Services at 760-750-4490.

- I received a Form 1098-T from CSUSM, do I qualify for an education tax credit?Not necessarily. Determination of eligibility is the responsibility of the taxpayer.

- How can I determine if I am eligible for an educational tax credit?You or your parents may be eligible for the educational tax credits on your tax return. For more details, you can read IRS Publication 970.

- The SSN or ITIN on my 1098-T is missing/incorrect. What should I do?Reporting to the IRS depends primarily on your SSN or Individual Taxpayer Identification Number (ITIN). It is very important for you to have the correct information on file with CSUSM. If CSUSM does not have an SSN on file, complete and return, in-person, to Cougar Central an IRS W-9 form (you will also need your SSN card and student ID card for identification purposes). To correct your SSN or ITIN, please contact Student Financial Services at 760-750-4490.

- Why didn’t I receive a Form 1098-T?

There are multiple reasons why you may not have received a 1098-T:

- If you received more scholarships and/or grants than the amount of qualified tuition and fees billed, CSUSM is not required to produce a 1098-T

- If you are classified as a non-resident alien, CSUSM is not required to produce a 1098-T

- Address inaccuracy (outdated or inaccurate address on file with CSUSM). If this occurred, you can update your information in your student center and access your 1098-T there as well. You can always request a replacement to be mailed by contacting Student Financial Services.

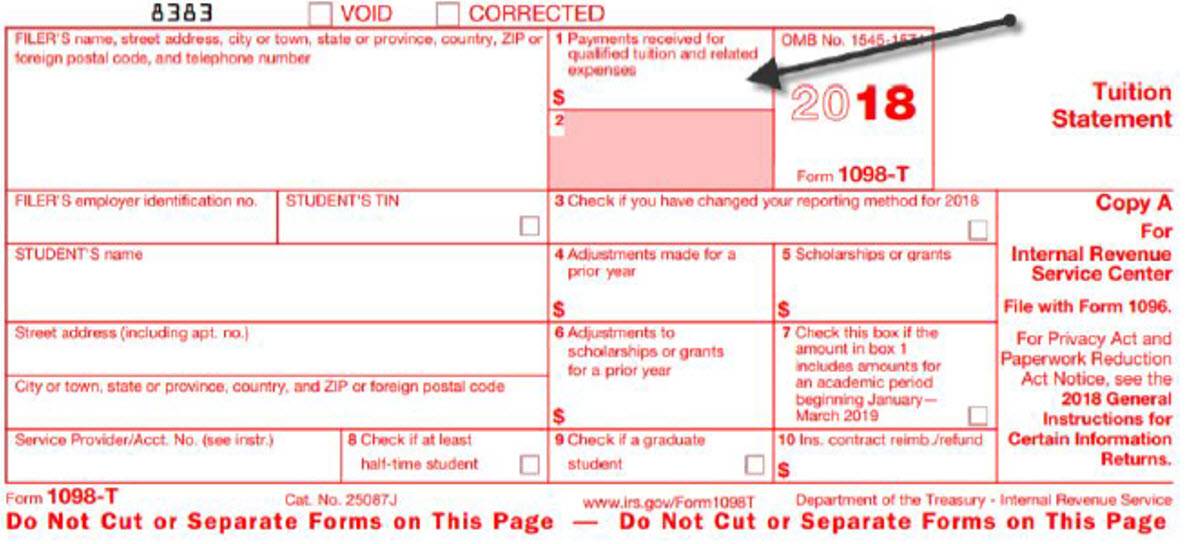

- What information is on Form 1098-T?

- Name, address, and taxpayer identification number for CSUSM

- Name, address, and taxpayer identification number of the student

- Whether the student was enrolled in at least half-time or full-time academic workload for at least one academic period

- Whether the student was enrolled exclusively in a graduate-level program

- Amount of qualified tuition and fees paid to CSUSM

- What Changed for 2018?Congress and the IRS eliminated the option for colleges and universities to report ‘Amounts Billed’ on Form 1098-T. Colleges and universities must now report ‘Payments Received’ for qualified tuition and expenses.

- What Does the 2018 Change Mean For You?

You will no longer see any amounts in Box 2 (Amounts Billed), but rather will have amounts displayed in Box 1 (Payments Received).

For the transition to ‘Payments Received’ for 2018, the potential for overlapping payments for the Spring 2018 term exists. The ‘Reported Method Changed’ indicator (Box 3) will be checked and notifies the IRS.

- What happens if I make a payment for the Spring term in December?

The data included on a Form 1098-T is based upon the calendar year, not academic year. If the payment is received and processed prior to January 1st, the payment will appear on that year’s 1098-T (not the next year, or upcoming academic year).

- What happens if I make a payment for the Spring term in December, but withdraw in

January?

The payment will remain on the current year’s Form 1098-T, but the following year’s form will report any refund associated with the December payment.

- My Box 5 Amount is Greater Than Box 1, is it Taxable?It may or may not be (dependent upon the source of funds). Please refer to IRS Publication 970.

- Are Payments From the VA Reported in Box 1?Payments from any source, except scholarships that cannot be used to cover Qualified Tuition and Related Expenses, are reported in Box 1, up to the amount of QTRE.

- A Third Party Paid My Tuition, How is This Reported on My 1098-T?Payments received from a third party are reported in both Box 1 and Box 5. Please speak with a tax adviser for how this impacts any potential tax credit, etc.

- I Received a Tuition Waiver, How Is That Reported on My 1098-T?Tuition waivers will reduce the sum of a student’s QTRE (Qualified Tuition and Related Expenses), therefore, it lowers the total potential tax credit available.

- What information is contained in the various boxes on the Form 1098-T?

- Box 1: The total payments received for qualified tuition and related expenses, less any related reimbursement or refunds.

- Box 2: No Longer Used

- Box 3: Any adjustments made to a prior year for qualified tuition and related expenses that were reported on a prior year Form 1098-T. This amount may reduce allowable education credit you may claim for the prior year. See IRS Form 8863 or Pub 970 for more information.

- Box 4: The total of all scholarships or grants administered and processed by CSUSM. The amount of scholarships or grants for the calendar year (including those not reported by CSUSM) may reduce the amount of any allowable tuition and fees deduction or the education credit you may claim for the year.

- Box 5: The adjustments to scholarships or grants for a prior year. This amount may affect the amount of any allowable tuition and fees deduction or education credit you may claim for the prior year.

- Box 6: If this box is checked, the amount in Box 1 or 2 included amounts for an academic period prior to the previous year. See IRS Form 970 for how to report these amounts.

- Box 7: The total amount of reimbursements or refunds of qualified tuition and related expenses made by an insurer. The amount of reimbursements or refunds for the calendar year may reduce the amount of any allowable tuition and fees deduction or education credit you may claim for the year.

- Box 8: Reveals whether you are considered to be carrying at least one-half the normal full-time workload for your course of study at CSUSM. If you are at least a half-time student for at least one academic period that begins during the year, you meet one of the requirements of the Hope Credit.

- Box 9: Reveals whether you are considered to be enrolled in a program leading to a graduate degree, graduate-level certificate, or other recognized graduate-level educational credential. If you are enrolled in a graduate program, you are not eligible for the Hope Credit, but you may qualify for the tuition and fees deduction or the lifetime learning credit.

- Was this information reported to the Internal Revenue Service (IRS)?Section 65050S of the Internal Revenue Code, as enacted by the Taxpayer Relief Act of 1997, requires institutions to file information returns to assist taxpayers and the IRS in determining the amount of qualified tuition and related expenses (qualified expenses) for which an education tax credit is allowable under section 25A (American Opportunity and Lifetime Learning Education tax credits), as well as other tax benefits for higher education expenses.

- Am I required to attach the Form 1098-T to my tax return?No. The primary purpose of the 1098-T is to inform you that CSUSM has provided the required information to the IRS to assist them in determining who may be eligible to claim the tuition and fee deduction or education credits. There is no IRS requirement that you claim a tuition and fees deduction or an education-related tax credit.

- I am unsure about 1098-T and filing my income tax. Who should I contact?CSUSM cannot provide tax or legal advice. Please seek advice from the IRS or a tax professional. Information is also available in the IRS Publication 970: Tax Benefits for Education.

- Where can I get a list of payments made to CSUSM?You can view payment details in the “Finance” section of your student center at MyCSUSM. Inside the “Finance” section, click “Account Inquiry”, then click the “Payments” tab. The “Payments” tab will contain a comprehensive list of all payments, by date, made to CSUSM.

- What are examples of charges/costs that are not included on my Form 1098-T?

This is a partial list:

- Housing

- Parking

- Meals

- Books

- Health Services/Health Facilities

- Mental Health

- I made payments on my student loans. Will you provide info on the amount of interest

paid?No. This information will be provided by your loan servicer on Form 1098-E.

- I need a copy of a Form 1098-T prior to this past calendar year, how can I get it?Prior year 1098-T information can be found in your student center. In the “Finances” section, click on the 1098-T link. The next page will reveal a link to each year you had a 1098-T from CSUSM.

More Information

California State University San Marcos does not assist in tax preparation, act as a tax consultant for individuals or entities, provide tax advice, and cannot answer your tax questions. Please consult a tax professional, the IRS, or a financial planner who is proficient with tax and tax laws. Each student and/or their parents must determine eligibility for, calculation of, and limitation of the tuition and fees deduction or the education credits (Hope of Lifetime Learning Credit).

While the University has made every effort to use the most current and accurate data, tax laws change frequently, and it is possible that some of the information may no longer be accurate. The university disclaims all liability from the mistreatment of information and materials contained in this document.

Information regarding immigration, employment, and tax substantial authority are the responsibility of each individual. Please keep in mind that no one from CSUSM, while in their official role at the university, can act as a tax consultant, give personal, legal, or tax advice, or represent an individual dealing with the Internal Revenue Service. Thus, any assistance the above information may provide is given as a courtesy to you, and as such, should not be construed in any way as the rendering of legal or tax advice.